A backdoor Roth IRA is a strategy that allows high-income earners to contribute to a Roth IRA even if they exceed the income limits for direct contributions. The strategy involves making non-deductible contributions to a traditional IRA and then converting those funds to a Roth IRA.

Benefits of a Backdoor Roth IRA

- Tax-free growth: Earnings in a Roth IRA grow tax-free, and qualified withdrawals in retirement are also tax-free.

- No required minimum distributions (RMDs): Unlike traditional IRAs, Roth IRAs do not have RMDs, which can provide greater flexibility in retirement.

- Estate planning: Roth IRAs can be a valuable estate planning tool, as they can be passed on to beneficiaries tax-free.

Drawbacks of a Backdoor Roth IRA

- Taxable conversions: Converting funds from a traditional IRA to a Roth IRA can trigger income taxes.

- Income limits: The backdoor Roth IRA strategy is only available to high-income earners who exceed the income limits for direct Roth IRA contributions.

- Five-year aging rule: Withdrawals from a Roth IRA are subject to a five-year aging rule, meaning that funds must be in the account for at least five years before they can be withdrawn tax-free.

Is a Backdoor Roth IRA Right for You?

Whether or not a backdoor Roth IRA is a good idea depends on your individual circumstances. Here are some factors to consider:

- Your income: If you exceed the income limits for direct Roth IRA contributions, a backdoor Roth IRA may be a good option.

- Your tax bracket: The tax implications of converting funds from a traditional IRA to a Roth IRA can vary depending on your tax bracket.

- Your retirement goals: If you are looking for a tax-advantaged retirement savings vehicle, a Roth IRA can be a good option.

How to Set Up a Backdoor Roth IRA

To set up a backdoor Roth IRA, follow these steps:

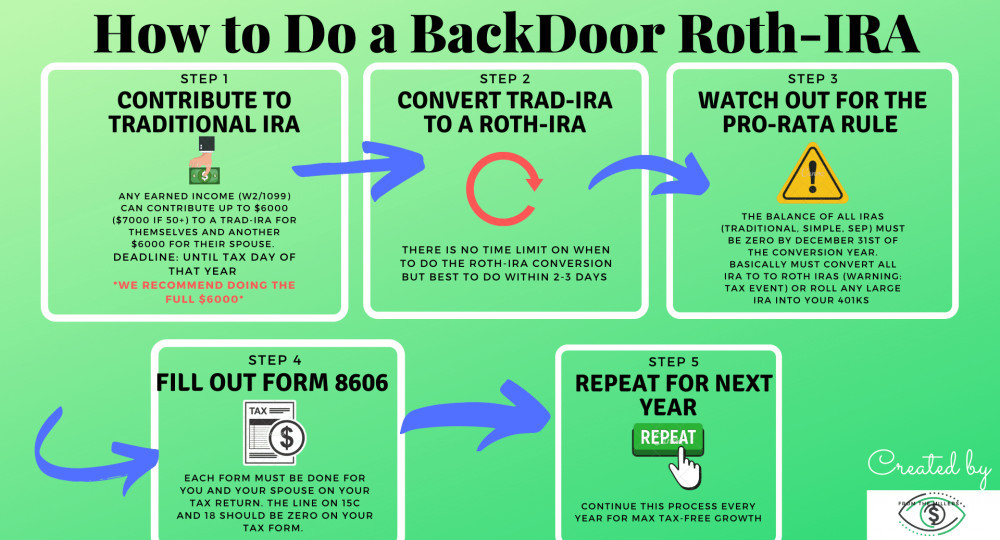

- Open a traditional IRA.

- Make a non-deductible contribution to the traditional IRA.

- Convert the funds from the traditional IRA to a Roth IRA.

A backdoor Roth IRA can be a valuable retirement savings tool for high-income earners. However, it is important to understand the potential tax implications and other factors before deciding if this strategy is right for you.

FAQ

Is backdoor Roth really worth it?

What is the 5 year rule for backdoor Roth IRAs?

What is the downside of Roth conversion?

Will back door Roth go away?

Could a backdoor Roth IRA benefit high-income earners?

A backdoor Roth IRA could benefit high-income earners. A “backdoor Roth IRA” is just a name for a strategy of converting nondeductible contributions in a traditional IRA to a Roth IRA. The strategy can be helpful for those who earn too much to contribute directly to a Roth IRA.

Is it worth doing a backdoor Roth IRA?

A backdoor Roth IRA is a strategy used by high-income earners to convert their traditional IRA to a Roth IRA without income or contribution limits . This strategy is beneficial for someone who

When can I make a backdoor Roth IRA contribution?

Note: A contribution using this backdoor Roth IRA strategy must be made by December 31 of the tax year in which a conversion happens. *Married (filing separately) can use the limits for single individuals if they have not lived with their spouse in the past year.

Is a backdoor Roth IRA a tax dodge?

The backdoor Roth IRA strategy is not a tax dodge. When you transfer the assets of a traditional IRA to a Roth IRA, you owe taxes on any funds—the principal, earnings, and appreciation—that have not been taxed previously. If the IRA was funded solely with tax-deductible contributions, then the entire value of the transferred assets is taxed.